THIS NEW FEDERAL LAW WILL PUT MONEY BACK ONTO YOUR BOTTOM LINE…IMMEDIATELY!

Most likely, you got to this presentation after receiving some information such as a business card or flyer with this link on it. Regardless of how you arrived, everything from this point forward is based on this article from the Federal Trade Commission:

and this “mission statement” from the former head at the time Congress passed these new rules:

As Mitchell Katz, spokesman for the Federal Trade Commission, said in May of 2011: The Dodd-Frank law prohibits a payment card network such as Visa “from inhibiting the ability of anyone to provide a discount for payment by cash, checks, debit cards, or credit cards,” said Katz. “Neither surcharging, nor a cash discount is illegal.”

It is also based on the 7.6 billion dollar lawsuit the Department of Justice filed against Visa, MasterCard, and American Express; which I will briefly cover in a moment.

First, let’s discuss a little bit about the credit/debit card processing industry from the reality of business owners. I am a business owner and I have/do require the services of merchant processing. I know what it’s like having to pay merchant fees. I also know there is not a single business owner or merchant, not just in America, but around the world that wants to pay merchant fees out of their profits when they can receive cash and pay no fees.

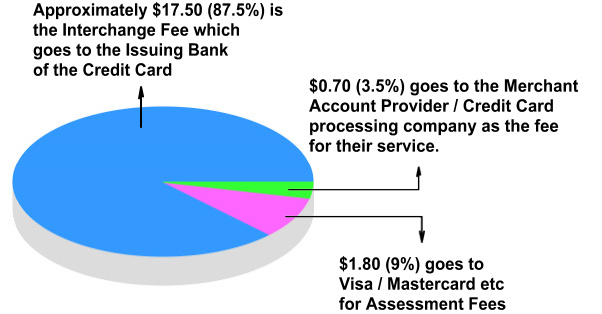

Second, until the Dodd-Frank Act, specifically, the Durbin Amendment; there has never been one single piece of legislation or any sort of legal governance over this industry. Visa, MasterCard, Discover, and American Express along with the member banks who own these associations, we’re only regulated by one thing and that is what they thought they could get away within the marketplace. That’s it. It was the merchants who paid the price and fell subject to this practice because the real outcome was how the banking industry (in addition to increasing Consumer Debt around the world), were able to take 2-12% of every business owners profit right off the top without investing in or loaning money to help that business owner.

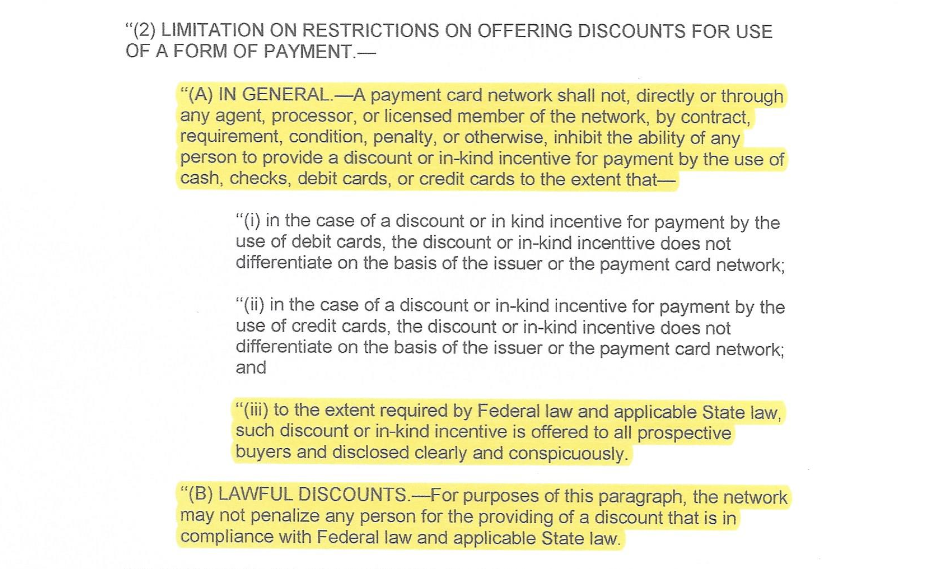

The Durbin amendment was 10 pages, but I’m going to focus on just what it says about recouping fees and expenses thereby putting that money back in your pocket. So, this is the Durbin Amendment:

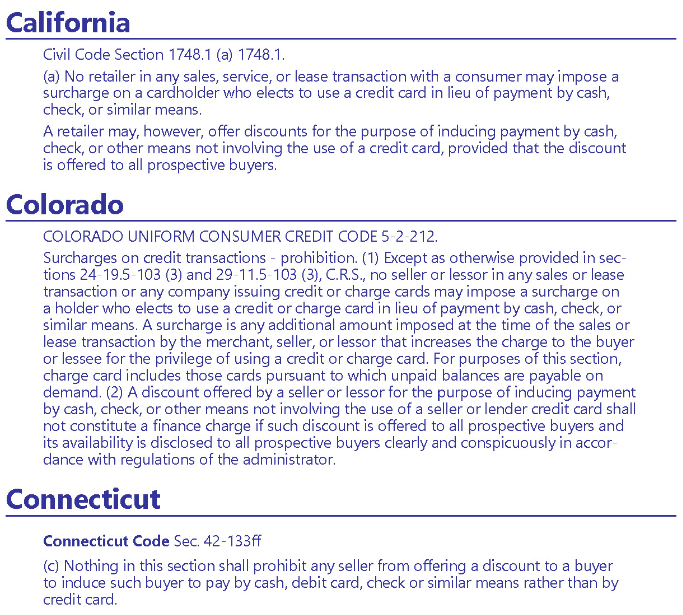

and this is some of the state regulations:

Now, the DOJ lawsuit which was mentioned and posted above was a massive class action. but, the real point of the lawsuit was to make the Card Network and the Associated Banks change the language of their contract. Before these new rules came into effect, having a contract with a Card Network meant if you were caught trying to recoup these expenses and fees by offering a discount for cash or any in-kind incentive (showing appreciation to a cash customer for going out of their way to bring you cash), you could be penalized and fined $10,000. Where did this penalty come from? Simple, it was in the contract which you never saw. But, you are assumed to have read and understood the contract the moment you process the first card. So any merchant that was caught or suspected of lowering a price for a cash customer would receive a fine in the mail from the Card Network; whether it was Visa, MasterCard, etc. If you didn’t pay it they simply cut off your service so that you can no longer take a card. If after that, you didn’t pay the fine, they send their attorneys after you and put you in the court to enforce the contract.

The simple point is (1) it’s unfair to cash customers due to convenience vs. inconvenience, (2) it has always been unfair to the business owner because it is not your convenience, and (3) in addition to everything else, Visa and MasterCard, along with all the banks; have made you a loan originator without any compensation. The good news is, that’s going to change because the legislation and the new rules are changing the entire merchant servicing industry. Like any change in legislation at a federal level, such as Obamacare, it may take 6 or 7 years for it to roll out completely to all the business owners. what that means for this particular industry and you is that those merchants who get on board first or going to save the most money because they’re first in line and first in time.

We’ve only been doing this for 18 months and we already have one merchant, who decided to think about it for a year then finally got on to the system, and recently gave us one of our best testimonials. He loves it. He’s saving money. That money is helping pay his rent, his insurance, and increasing his bottom line by recouping this unneeded expense.

Like all of our clients who have been on Our system for a year or more, no one’s losing any customers. From our perspective, even when a business owner says they are worried about a loss in customers, the only question is where are they going to go? Give me the names of where you think you’re going to lose business and to who. We’ll go sign them up and put everyone on the system. That way no one loses any of their customers because this is going to happen anyway.

Governmental legislation that affects business always changes an entire industry. Changing the card processing industry because it was taking advantage of business owners is the entire purpose of this change in legislation. Because, without business owners who employ people, the Federal Government has no one to tax. As stated before, I am a business owner. I did not get involved in this industry because I saw a change and an opportunity, I got involved because I have an overall care for other business owners because I know that without business owners the Federal Government is unable to collect any taxes. Business owners run everything because they are the ones that employ the other taxpayers that don’t want to be in business.

So, now that the truth is on the table, let’s talk about the final truth which is, who should be paying card processing fees? Should it be a third party like the business owner or should it be the cardholder whose name is on the account? Should anyone (business owners and consumers alike) ever have to pay a fee at your point of sale cash register for the privilege of taking someone else’s card; which is a convenience for them and an inconvenience for you? That’s a rhetorical question because we already know that no business owner wants to pay the fee because it’s a deduction from their bottom line profits. The truth of the matter is, Visa, MasterCard, American Express and the banks have made enough money off of this just in the massive increase in Consumer Debt and never needed to charge a fee on top of it.

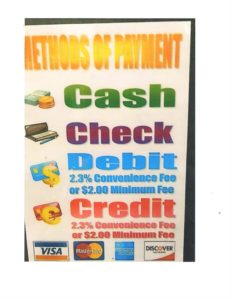

To conclude; let’s talk about our program and whose already doing this. Being a new governmental rule, the first people to jump on board was the government. This is a copy of a sheet of paper that’s posted at a DMV next to every terminal where they accept payment. They show four options; cash, check, debit, or credit. For cash or

The gas companies were next (probably because they were instrumental in getting the legislation passed through their lobbies) where you see this rolling out at stations charging anywhere between 5-15 cents more per gallon at the pump for the consumer that uses a card versus walking in the store and giving the teller cash. Utility companies and universities are also passing on these fees to the cardholder.

Bottom line is this way of accepting payments and passing on the responsibility for such fees to the cardholder is not going away. The only question that needs to be asked is when are you going to get on board and start putting money back into your pocket?

TESTIMONIALS FROM EXISTING MERCHANTS ON OUR PROGRAM

Saving $300.00/Month Avg!

Saving 10k per year!

Cash Sales have increased!